by Bernhard Ebbinghaus

- Every fourth person in Europe receives an old age, survivor or disability pension benefit, an automatic stabilizer during this crisis

- Public pay-as-you go pension will soon come under severe pressure due to fiscal pressures accelerated during this pandemic

- Private funded pensions with their additional risks, were hit hard after the 2008 crash and will again increase inequalities in old age in coming years

- Older people transitioning from work to retirement will face immediate difficulties that need to be addressed

While the elderly are currently in the news as the main Covid-19 risk group with higher fatality rates, most of the economic and social impact analyses focus on the working age population, hardly on retirees. Certainly, during the pandemic, public pensions will guarantee retirees a smooth income stream while working people fear losing their job, face earnings cut due to short-time work or might need to work at home while caring for children or other family members in need of care.

This perspective might be short-sighted, ignoring some short and long-term consequences for older people in retirement. While pensions are automatic stabilizers in times of an economic crisis, benefiting a quarter of the population in Europe, their financial sustainability maybe at considerable risk tomorrow. Increasingly, advanced economies have moved towards private pillars, particularly funded pensions, be it occupational or personal pensions, shifting risk to individuals.

The impact of an economic crisis on pensions

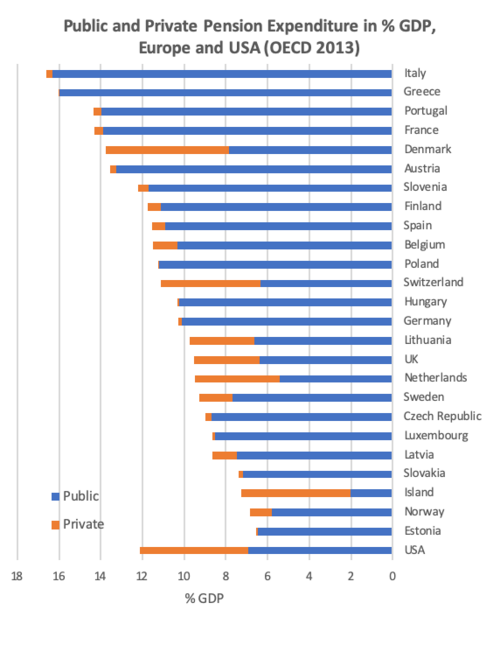

The Great Recession instructs in respect to the positive side of pensions but also its many challenges on retirement income. During the last crisis, public pensions were automatic stabilizers, guaranteeing income of about every fourth person through old age, survivor or disability pensions. Pension expenditures are the largest — nearly half (45%) of all social expenditures across the European Union, and many Continental countries spend more than 10% of GDP on public pensions (see Figure 1). Since the 2008 crash, old age poverty declined relative to working age income as joblessness hit households more severely, but subsequently, when unemployment declined, old age poverty climbed again. During the pandemic a similar relative change of working age versus older population will occur again if the recession persists for several years.

Figure 1

Due to the Great Recession and subsequent Euro Sovereign Debt crisis, governments were under pressure to further reform their public pensions, increasing the retirement age and cutting back on future benefits. Not least the bailout of financial institutions and the large stimulus packages were very costly then. In addition to demographic ageing, declining tax revenue and social contributions, at a time of rising welfare costs for the jobless, added to the fiscal squeeze.

Particularly crisis-ridden countries in Southern Europe, Ireland and several newer EU member states saw their public debt skyrocket. Before the pandemic (2019Q3), UK had just under 85% in public debt, Germany at 62% around the Maastricht benchmark, while the Eurozone (EA19) had similar levels to the UK, however, with big variations—from Greece (178%), Italy (137%) and Portugal (121%) to Luxembourg (20%) and Estonia (9%). The current coronavirus spending packages will significantly increase public debt for many years to come, and it will be particularly difficult for Italy and Spain hit massively by the Covid-19 outbreak and early lockdown.

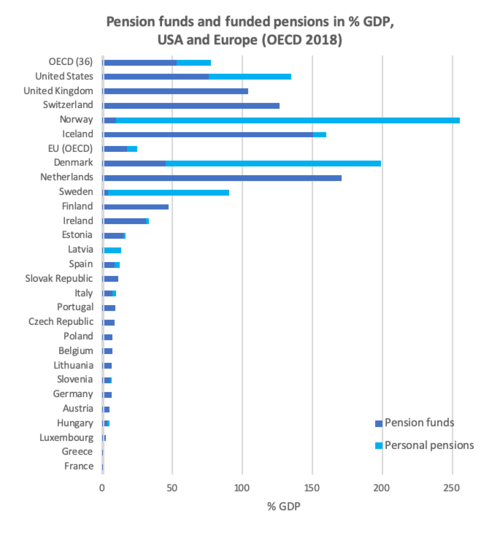

While the automatic stabilizer function weights on the positive side of pensions, there were also immediate negative effects following the last crisis. When the stock market crashed in 2008, this led – within a year – to OECD pension fund assets declining by 20% (10% per country average, up to 30% in Ireland). After a decade, not all funds had fully recovered and average annual growth rates were only around +3% across the OECD. By early April 2020, following the onset of the coronavirus, the Dow had fallen by 10%, FTSE100 by 20% and Euro Stoxx by 15% over the previous year, demonstrating a crash similar to 2008/09. Again, if the recession continues, we should expect similar impacts on pension funds and individual savings, these will likely be particularly severe if multi-pillar pension systems are “mature” (see top countries in Figure 2).

Figure 2

Lessons from the last crisis

Occupational pensions with defined benefits (DB) will see their liabilities go up in annual evaluations, raising red flags for pension regulators. These will require a rebalancing via employer contributions and painful benefit cuts for future and/or current beneficiaries. Additionally, bankruptcy of companies is a problem even with protective reinsurance, leading to increased premiums. As a consequence, in countries with large occupational schemes such as in Great Britain, the Netherlands, and Switzerland, governments and regulators intervened in the last crisis to mitigate effects. A further consequence was that ever more employers closed down their DB schemes to new entrants. Given the unprecedented pressures on business during the coronavirus crisis, similar liability problems, the pressure of failing funds, and long-term withdrawal will happen again. If occupational pensions are negotiated, employers and unions will have to make tough decisions in a difficult business environment.

While occupational pensions still allow some collective risk pooling and employer responsibility, the personal pensions with a defined contribution (DC) saving plan have fully individualized risks. Depending on the investment portfolio, individual retirement savings might be affected by negative asset returns, and they often lack professional fund management and the risk pooling of pension funds. Those pensioners who kept retirement savings in more risky investments will be hurt most, whereas those who have bought an annuity or shifted toward more conservative investments are better sheltered. The same holds for those nearing retirement and who have not opted for a life cycle investment strategy. They might be forced to work longer at a time when joblessness, income cuts and insecure working conditions prevail.

Given the inadequacy of pensions to maintain the standard of living, a considerable share of pensioners are working extra hours to increase their disposable income, though nearly half of working pensioners do this for non-financial reasons. Around 20% of older people aged 65-69 are working across all OECD countries, including Germany (17%) and the UK (21%). Although many are self-employed or work part-time, it will be difficult for them to maintain their work-related income level during the recession. As many countries have increased pensionable age, not least advanced over the last decade in response to the last economic crisis, older workers will have to work even longer even as they may face particular challenges due to unexpected dismissal and limited reemployment opportunities. Many reforms have limited or even closed down the pathways to early exit from work. Those forced to retire involuntarily due to disability or dismissal will be negatively affected by more meagre benefits.

The immediate short-term effects may be more limited for some groups, such as those facing retirement during the coming months, the current “working pensioners”, and those retirees with risky investments. However, the long-term consequences for both public pensions and funded private schemes look bleak, not least since the increased risks – visible after the last crisis – seem to have been ignored on political agendas.

Public pensions may serve as automatic stabilizers, yet already during the immediate crisis, social contributions and tax revenues will decline due to mass underemployment and low business activities. Concerns about the financial sustainability of pay-as-you go pensions are not just fuelled by demographic ageing but also any recession. Already for several decades, the pay-as-you go pensions in Southern Europe have been criticized for being financial unsustainable: These rapidly ageing countries suffered dramatically from the last crisis. The pandemic will increase further pensions reforms due to increased public debt. In countries with public minimum income provisions for the elderly, keeping old age poverty in check will depend on the generosity of basic pensions and the importance of other private pillars in retirement income.

The impact will be differential, depending on the pension system in place. Many continental European pension systems with Bismarckian social insurance will likely face the challenges of pay-as-you go financial unsustainability. Several of these countries as well as Eastern European countries moved to voluntary or even mandatory funded pensions in the 1990s, though the level of current beneficiaries is small, as are the accumulated assets (Estonia is on top with 15% of GDP in pension fund assets). Moreover, some countries have lowered contributions during the Great Recession or even nationalized its funded pillar (Hungary). In systems with basic pensions or means-tested pensions, the demand for income security will become larger while the capacity of the state to finance these will be severely taxed in years to come. In all public pension systems, as in the last crisis, a reluctance to increase pensions will become widespread. Further pensions reforms are waiting as financial (un)sustainability will drive the agenda again instead of social adequacy and safety net concerns for older people.

In contrast, funded pensions (OECD, see Figure 2) have been particularly important pillars in Beveridge-type pension systems, with substantial pension fund assets (%GDP in 2018) such as the Netherlands (178%), Iceland (150%), Switzerland (127%), and Britain (105%). A 10 to 20% decline in assets of such funds during one or two years of the pandemic would have important macro-economic effects. It would also substantially reduce individual DC savings and the weight on the liabilities of company or sector-level DB schemes. Given the share of current retirement income that is already dependent on returns in these mature multi-pillar systems, the repercussions could be relatively severe in the short and medium-term for those close to or in retirement. Some funded pension systems have weathered the last crash better than others, such as Danish group insurance with little effect contrasted with risky Irish pension funds. Whether these systems have learnt any lessons and will weather this storm any better than the last is difficult to predict now, given the uncertainties associated with the viral spread.

Just like the 2008 crash, the current stock market led to major asset losses within weeks of the global pandemic, repeating the negative impact on pension funds and individual saving plans. While those close to retirement may have to postpone their decision while facing job loss, catastrophic for some, also pensioners who have not annuitized their savings prior to the crash will face major shortfalls. Many working pensioners, forced to work to attain a decent living, may lose their extra income as they are laid off or quit, not least due to their higher health risks in this pandemic. In conclusion, the lessons from the last economic crisis, the Great Recession, indicate that both public pensions and funded old age savings will be adversely affected – with considerable consequences for more than a quarter of the population. Even if currently less visible than the immediate threat to life, these challenges need attention now to avoid dire situations in coming decades.

About the Author

Bernhard Ebbinghaus is Professor of Social Policy, Head of the Department of Social Policy and Intervention and Senior Research Fellow of Green Templeton College at University of Oxford.